Business license tax is a mandatory tax imposed on organizations and individuals engaged in production and business activities in Vietnam. This is a fixed annual fee, categorized based on the taxpayer’s charter capital or revenue. Understanding business license tax helps businesses and individual business households comply with legal regulations, avoid declaration errors, and prevent penalties. Notably, under current regulations, there are 10 cases exempt from business license tax, reducing the financial burden for certain groups. This article provides detailed information on business license tax, calculation methods, declaration procedures, and the latest tax exemption cases.

What is Business License Tax? Who is Required to Pay It?

Definition of Business License Tax

Business license tax is a direct tax applied to organizations and individuals engaged in business activities in Vietnam. It is a fixed annual tax collected to regulate business operations and generate revenue for the state budget. Currently, the official term used in legal documents is “business license fee” instead of “business license tax.” However, many businesses and individuals still refer to it by its former name. Understanding business license tax is crucial for businesses to ensure compliance with legal regulations and avoid unnecessary penalties.

Subjects Liable for Business License Tax

According to current regulations, the following entities are required to pay business license tax:

- Enterprises established under the Law on Enterprises, including joint-stock companies, limited liability companies, and private enterprises.

- Individual business households with annual revenue of 500 million VND or more.

- Branches, representative offices, and business locations of enterprises.

- Other economic organizations engaged in the production and trading of goods and services.

Current Business License Tax Rates

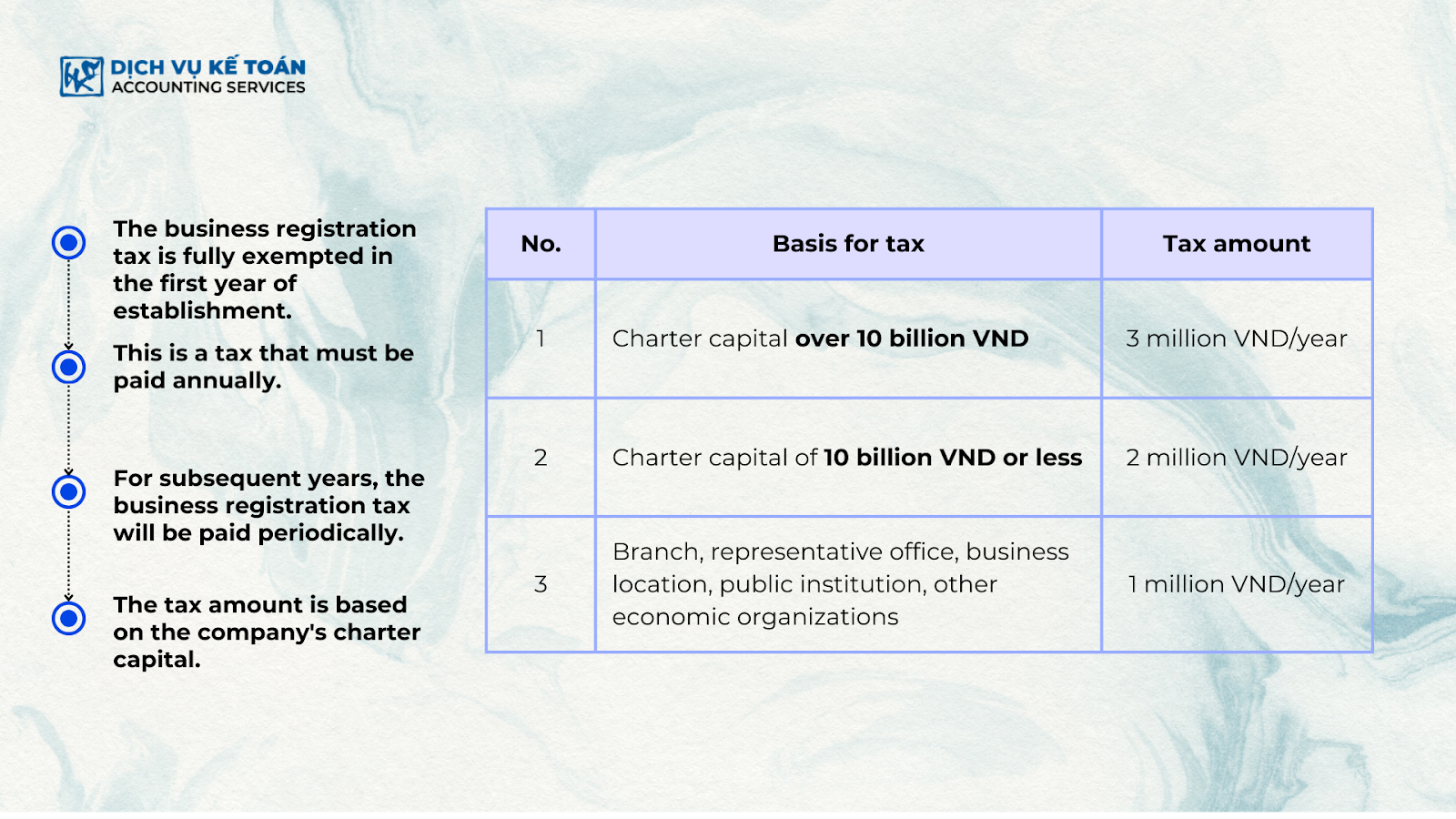

The business license tax is determined based on charter capital for enterprises and revenue for business households:

- Enterprises with charter capital over 10 billion VND: 3,000,000 VND/year.

- Enterprises with charter capital of 10 billion VND or less: 2,000,000 VND/year.

- Individual business households with annual revenue over 500 million VND: 1,000,000 VND/year.

Business License Tax Payment Deadline

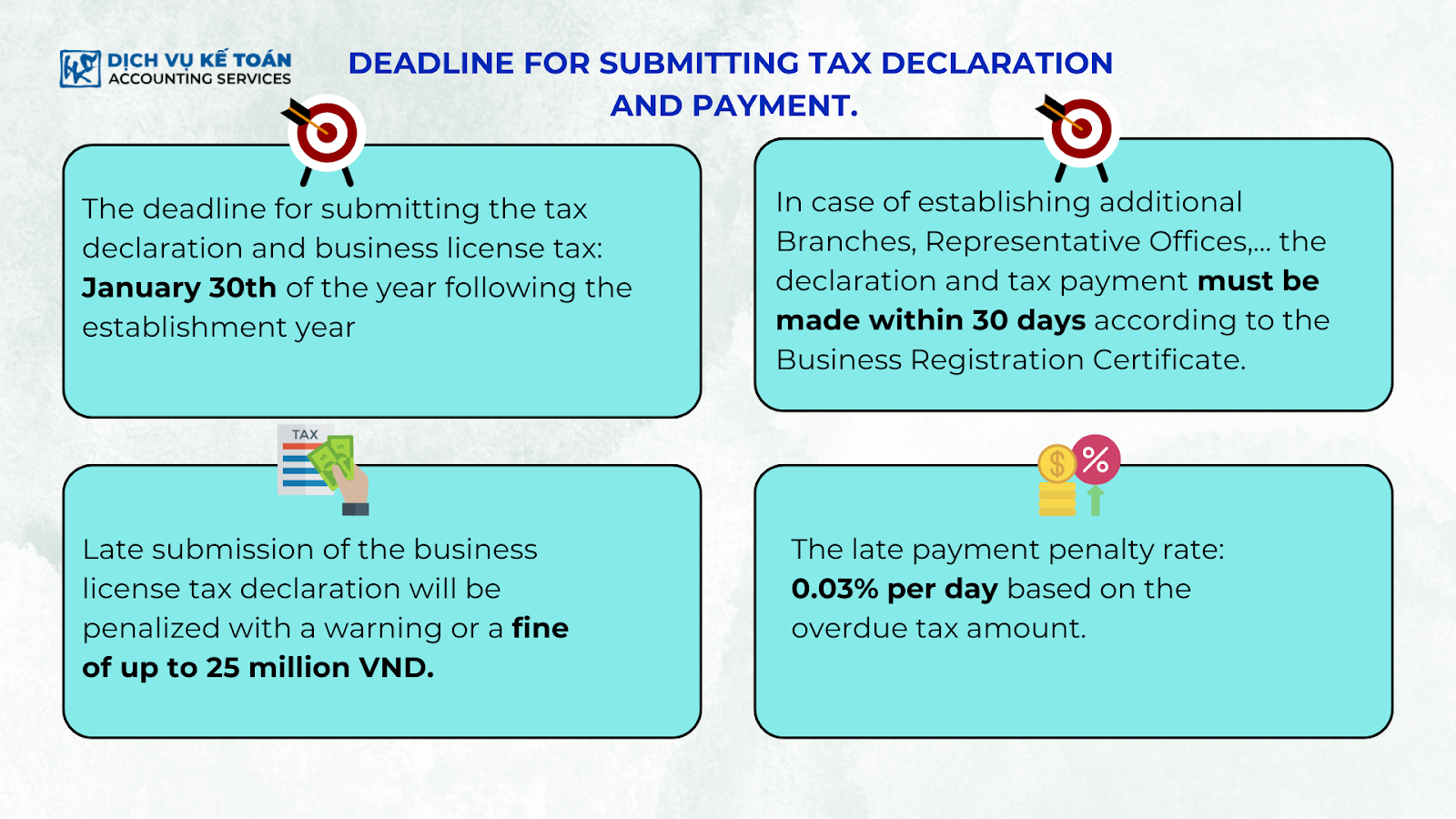

- Enterprises and organizations must pay the business license tax before January 30 each year.

- For newly established enterprises, the deadline for business license tax payment is within 30 days from the date of issuance of the business registration certificate.

Learn more: Types of Taxes Businesses Must Pay After Establishment

How to Calculate Business License Tax Under the New Regulations

Formula for Calculating Business License Tax

Business license tax is calculated based on the charter capital of enterprises or the annual revenue of business households. The specific tax rates are stipulated in decrees and circulars issued by the Ministry of Finance to ensure transparency and fairness in the tax system.

- Enterprises apply the tax rate based on their initial registered capital.

- Business households determine their tax liability based on their annual revenue.

Accurately determining the amount of business license tax helps businesses comply with legal regulations and avoid risks related to incorrect tax declarations or late payments.

How to Determine Capital for Tax Calculation

The amount of business license tax payable is determined based on two key factors:

- Charter capital (for enterprises)

- Annual revenue (for business households)

- For enterprises: The charter capital recorded in the business registration certificate is the basis for tax calculation.

- Capital over 10 billion VND → 3,000,000 VND/year

- Capital of 10 billion VND or less → 2,000,000 VND/year

- For business households:

- Revenue over 500 million VND/year → 1,000,000 VND/year

Guidelines for Declaring and Paying Business License Tax

Business license tax declarations can be submitted via the General Department of Taxation’s online portal. Enterprises can choose to:

- Declare and pay online through electronic tax payment services.

- Submit tax payments directly at the State Treasury.

For online tax payments, businesses must have a bank account and be registered for electronic tax services.

Late or incorrect declarations may result in administrative penalties.

Penalties for Late Payment of Business License Tax

If an enterprise or business household fails to pay the business license tax on time, penalties will apply. The fines range from 1,000,000 VND to 5,000,000 VND, depending on the duration of the late payment. To avoid penalties, businesses should carefully track tax deadlines and ensure timely tax payments.

10 Cases Exempt from Business License Tax Under the New Regulations

Business license tax exemptions help reduce financial burdens for certain business entities. According to current regulations, 10 cases are eligible for business license tax exemption, including:

- Individuals and households with annual revenue under 100 million VND: This policy supports small-scale businesses, allowing them to operate without tax pressure.

- Households with irregular business activities and no fixed location: Small vendors and businesses without a fixed business location are exempt from this tax.

- Salt production: Individuals and households engaged in salt production are exempt to encourage industry growth.

- Aquaculture and fishing: Households and individuals involved in aquaculture and fishing are not required to pay business license tax.

- Communal cultural post offices and press agencies: These organizations are exempt to support cultural and media activities.

- Agricultural cooperatives: Agricultural cooperatives are exempt to promote agricultural production.

- People’s credit funds in mountainous areas: Financial organizations operating in mountainous regions are exempt to support underprivileged communities.

- Newly established businesses: New businesses are exempt from business license tax in their first year to help stabilize their operations.

- Small and medium-sized enterprises (SMEs) transitioning from household businesses: These businesses are exempt from business license tax for the first three years to encourage business transformation.

- Public primary and preschool education institutions: Public schools are exempt from business license tax to ease their financial burden.

Important Notes When Declaring Business License Tax

Common Mistakes in Tax Declaration

When declaring business license tax, enterprises and business households often encounter several common errors, such as:

- Incorrect tax amount declaration

- Missing important information

- Late submission of tax declaration forms

- Failure to register for a tax code on time, which may result in penalties from tax authorities

To avoid these mistakes, businesses should thoroughly understand the regulations, regularly check their tax declarations, and ensure they follow the tax office’s instructions correctly.

How to Correct Errors in Business License Tax Declaration

If an enterprise realizes that it has incorrectly declared business license tax, it can make adjustments by submitting a supplementary tax declaration form via the electronic tax filing system of the General Department of Taxation.

- Corrections should be made as soon as possible to avoid penalties for incorrect declarations or late payments.

- If businesses experience difficulties in making corrections, they can contact the local tax authority for detailed guidance.

How to Check Business License Tax Online

Checking business license tax information online allows enterprises to:

- Verify the exact amount due

- Check the status of tax declarations

To check business license tax information online, businesses can:

- Visit the General Department of Taxation’s electronic portal

- Enter their tax identification number (TIN)

- Follow the on-screen instructions

Using this online tool helps businesses ensure timely tax compliance and avoid penalties for late payments or incorrect declarations.

Important Changes in Business License Tax Regulations

Business license tax regulations may change annually based on government policies. Therefore, businesses must regularly update themselves with the latest information from the Ministry of Finance or local tax authorities to avoid mistakes in tax declaration and payment.

Key changes may include:

- Updated tax rates

- New exemptions from business license tax

- Changes in tax payment deadlines

Understanding and implementing these updates correctly will help businesses comply with legal regulations and optimize tax costs.

Business license tax is a crucial tax obligation that all businesses and business households must understand to comply with regulations properly. Timely tax declaration and payment help businesses avoid legal and financial risks.

Additionally, tax exemptions for specific cases support the growth of certain industries and business groups in the economy.

To ensure compliance and optimize tax costs, businesses should:

- Stay updated on new regulations

- Consider using professional accounting services for tax declaration and compliance assistance

For any inquiries, contact Wacontre Accounting Services via Hotline: (028) 3820 1213 or email info@wacontre.com for prompt assistance. With a team of experienced professionals, Wacontre is committed to providing dedicated and efficient service. (For Japanese clients, please contact Hotline: (050) 5534 5505).