Personal Income Tax (PIT) is a direct tax applied to individual incomes, playing a significant role in the state budget. Understanding the concept and methods of calculating PIT will help you fulfill your tax obligations correctly while optimizing personal finances. This article provides a guide to PIT calculation, legal regulations, and applicable updates for 2024.

What is Personal Income Tax?

Definition of PIT

Personal Income Tax (PIT) is a tax individuals must pay on earnings derived from sources such as salaries, capital investments, capital transfers, and others. PIT not only ensures revenue for the state budget but also acts as a tool to balance income distribution within society.

Taxpayers Subject to PIT

In Vietnam, PIT applies to two categories of taxpayers:

Taxable personal income

How to Calculate Personal Income Tax Accurately

PIT Calculation Formula

The amount of PIT payable is calculated as:

PIT Payable = Taxable Income × Tax Rate

Taxable Income: Income remaining after deductions for exemptions and family circumstances.

Tax Rate: Determined based on a progressive tax scale

Progressive Tax Rates

The current PIT progressive tax scale consists of seven brackets, with rates ranging from 5% to 35%:

Deductions When Calculating PIT

Deductions include:

- Family deductions: Personal deduction: 11 million VND/month và 4.4 million VND/month per dependent.

- Mandatory insurance contributions: Social insurance, health insurance, and unemployment insurance.

- Charitable contributions: Allowed deductions if proper documentation is provided

New PIT Regulations for 2024

Exemptions from PIT

Some cases of PIT exemption under the latest regulations include:

- Property transfers between related individuals (e.g., spouses, parents, and children).

- Thu nhập từ quà tặng, thừa kế giữa các thành viên gia đình.

- Thu nhập từ tiền làm thêm ngoài giờ, ca đêm (theo mức cao hơn giờ hành chính).

Tax Periods and Applicable Rates

Depending on the taxpayer and income source, the tax period may be:

– Annual basis: Income from salaries and business activities for resident individuals.

– Per occurrence: Applicable to other income sources such as capital transfers, real estate transactions, and winnings.

– Monthly or annual basis: For securities transfers, based on the taxpayer’s choice.

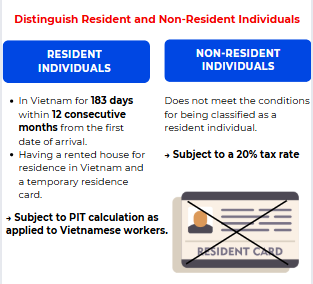

Conditions for Determining Residency

According to Circular 111/2013/TT-BTC, an individual is classified as a resident if:

- They are present in Vietnam for at least 183 days in a calendar year.

- They have a regular place of residence as defined by residency laws or a lease contract for 183 days or more.

Important Notes for PIT Filing

Deadlines and Filing Methods

- Filing Frequency: Monthly or quarterly, depending on business size.

- Submission Deadline: By March 31 of the following year for income from salaries and business activities.

Tools for Tax Filing

- Electronic Tax Filing Software: Enables easy submission of declarations and information retrieval.

- Online Tax Portal: Facilitates regulation lookups and swift tax filing.

Tips to Avoid Errors in Tax Filing

- Verify all documents: Ensure all incomes and deductions are fully declared.

- Plan periodic payments: Maintain schedules to meet deadlines and avoid penalties.

- Stay updated with regulations: Helps ensure compliance and adjust to changes promptly.

Understanding personal income tax regulations, new updates, and calculation methods enables you to meet tax obligations effectively while complying with the law. Regularly update your knowledge and use available tools to streamline the filing process and minimize legal risks.

Learn more:

Corporate Income Tax (CIT): Proper Understanding and Optimizing Efficiency

WHAT IS VAT? ESSENTIAL INFORMATION ACCOUNTANTS SHOULD KNOW ABOUT VALUE ADDED TAX (VAT)

For any inquiries, contact Wacontre Accounting Services via Hotline: (028) 3820 1213 or email info@wacontre.com for prompt assistance. With a team of experienced professionals, Wacontre is committed to providing dedicated and efficient service. (For Japanese clients, please contact Hotline: (050) 5534 5505).