Value Added Tax (VAT) is an integral part of Vietnam’s tax system. It is an indirect tax levied on the added value of goods and services throughout the production and consumption process. Understanding VAT not only helps businesses comply with the law but also optimizes tax costs and enhances operational efficiency. This article provides essential and up-to-date information about VAT, including its definition, calculation methods, and current legal regulations.

What is Value Added Tax (VAT)?

Definition of VAT

Value Added Tax (VAT), also known as “Thuế Giá Trị Gia Tăng” (GTGT) in Vietnamese, is an indirect tax levied on the added value of goods and services at various stages of production and distribution. This tax is typically collected by businesses on behalf of the government through the sale of goods or provision of services. Simply put, VAT is the tax consumers pay when purchasing goods or services, but businesses are responsible for remitting it to the tax authorities. In Vietnam, VAT has long been implemented and plays a significant role in ensuring state budget revenue while promoting transparency in business activities.

Characteristics of VAT

- Indirect Taxation: VAT is an indirect tax, meaning that the ultimate tax burden falls on the final consumer, while businesses act as intermediaries, remitting the tax to the government. This makes tax collection more efficient and reduces the risk of tax evasion.

- Applied to Added Value: VAT is calculated based on the value added at each stage of the supply chain, from production to final consumption. This characteristic distinguishes it from other taxes, such as excise tax or import-export duties.

History and Role of VAT

VAT was first introduced in France in the 1950s and quickly became a globally adopted tax model. Its primary role is not only to generate revenue for the state budget but also to encourage transparency in economic activities. In Vietnam, VAT was officially implemented in 1999 and has since become one of the key pillars of public finance, contributing to economic development and improving public infrastructure.

Differences Between VAT and Other Taxes

One of the key differences between VAT and other taxes lies in the tax collection mechanism. VAT is applied at each stage of the supply chain, from production to consumption, whereas taxes like excise tax are imposed only on specific goods. Moreover, VAT encourages transparency because businesses are required to issue invoices to claim input tax deductions, improving control and reducing tax fraud.

Cases Subject to VAT

Goods and Services Subject to VAT

Most goods and services in Vietnam are subject to VAT, ranging from food and clothing to services such as transportation and telecommunications. However, the VAT law also specifies exemptions, such as education, healthcare services, or imported goods used for humanitarian aid. Understanding this list helps businesses and consumers recognize their rights and obligations, avoiding penalties due to a lack of knowledge.

VAT Exemptions

VAT exemptions apply to specific goods and services to encourage the development of priority sectors, such as healthcare, education, and scientific research. Additionally, projects in agriculture or clean energy production may also qualify for VAT exemptions to promote sustainable development. Regularly updating exemption regulations helps businesses optimize operational costs.

Latest Regulations on VAT Liability

According to the latest regulations, not only business entities but also small-scale individual businesses are subject to VAT. This expansion broadens the tax base and ensures fairness in taxation. However, small businesses with annual revenue below VND 100 million may qualify for VAT exemptions or be taxed using a simplified direct method.

Benefits of VAT for the Economy

VAT contributes directly to state revenue while promoting transparency and accountability in business activities. Its application enables tax authorities to better monitor commercial activities and encourages businesses to improve productivity and product quality to add value.

Detailed VAT Calculation Methods

Tax Deduction Method

The tax deduction method is widely used, particularly by large-scale enterprises with stable revenues. Under this method, the VAT payable is calculated as:

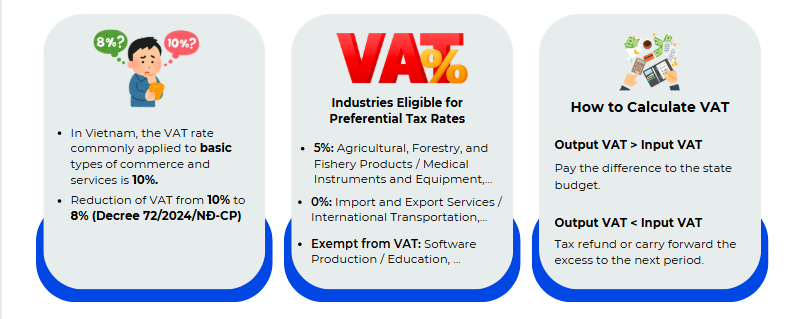

VAT Payable=Output VAT−Input VAT

Businesses must maintain proper invoices and valid documents to ensure their right to deductions. This method encourages transparency in business operations and strengthens financial management capabilities.

Direct Calculation Method

This method is typically applied to small household businesses or enterprises that do not meet the conditions for the deduction method. The VAT payable is calculated by multiplying the revenue by a specific percentage. For example:

- Construction services without material supply: 5% VAT rate.

- Manufacturing or transportation activities: 3% VAT rate.

While simpler, this method offers less incentive for businesses to professionalize and expand.

Current VAT Rates

Vietnam currently applies three main VAT rates:

Practical Example of VAT Calculation

A manufacturing business sells products with a pre-VAT price of VND 200 million. With a 10% VAT rate:

Output VAT = 200 million × 10% = 20 million VND.

If the business has purchase invoices with input VAT of VND 5 million, the payable VAT is:

Payable VAT = 20 million VND − 5 million VND = 15 million VND.

This clear calculation ensures compliance and financial accuracy.

VAT Refund: Regulations and Conditions

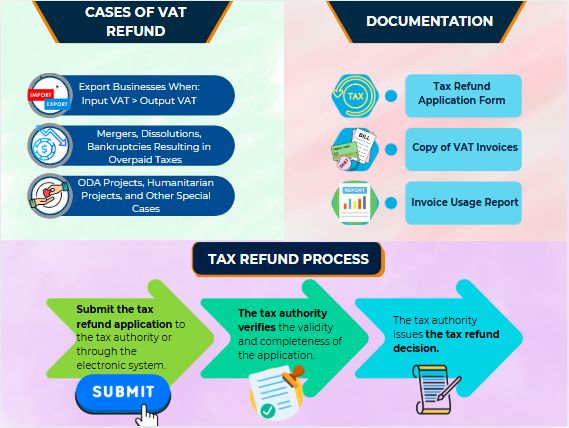

Cases Eligible for VAT Refund

VAT refunds apply in the following cases:

- Export businesses where input VAT exceeds output VAT.

- Mergers, dissolutions, or bankruptcies resulting in overpaid taxes.

- Special cases regulated by tax authorities, such as projects funded by ODA or humanitarian aid.

VAT Refund Process

The VAT refund process typically includes the following steps:

- Businesses submit the tax refund application to the tax authority or through the electronic system.

- The tax authority verifies the validity and completeness of the application.

- If eligible, the tax authority issues the tax refund decision.

This process requires strict adherence to regulations to avoid rejection.

Required Documents and Procedures

A VAT refund application must include:

- A tax refund request form (as per the official template).

- Copies of VAT invoices or related documents.

- An invoice usage report.

Documents must be carefully and accurately prepared to prevent errors during processing.

Tips to Avoid Mistakes During VAT Refunds

- Ensure invoices and related documents are valid and match the tax reports.

- Stay updated on changes in tax policies to proactively manage financial compliance.

Value Added Tax (VAT) is not only an essential financial tool but also reflects a business’s transparency and responsibility in its operations. Understanding VAT calculation, taxable entities, and refund procedures helps businesses comply with legal regulations while leveraging tax policies to optimize costs. For further information or assistance, feel free to contact our team of experts for timely and detailed guidance!

Learn more:

Corporate Income Tax (CIT): Proper Understanding and Optimizing Efficiency

Personal Income Tax: Definition and Calculation Methods

For any inquiries, contact Wacontre Accounting Services via Hotline: (028) 3820 1213 or email info@wacontre.com for prompt assistance. With a team of experienced professionals, Wacontre is committed to providing dedicated and efficient service. (For Japanese clients, please contact Hotline: (050) 5534 5505).