From 2025, exemption of corporate income tax for the first 3 years for newly established companies. Preferential policies help businesses start smoothly and develop sustainably. The policy from 2025 of exempting corporate income tax for the first 3 years for newly established companies opens up great opportunities for young businesses. With incentives such as exemption of corporate income tax in 2025, tax incentives for newly established companies, this is a strong motivation for successful startups.

From 2025, exemption of corporate income tax for the first 3 years for newly established companies

According to Resolution 68-NQ/TW, Section III, Sub-section 2.1 issued on May 4, 2025: abolishing business license fees, exempting corporate income tax for small and medium-sized enterprises in the first 3 years of establishment.

Thus, the policy of exempting corporate income tax (CIT) in the first 3 years will be applied to newly established small and medium-sized enterprises. The main subjects are enterprises registering for business for the first time, never operating before (including private enterprises, LLCs, joint stock companies and legally registered cooperatives).

In particular, the policy focuses on areas that encourage development such as high technology, technological agriculture, creative services, clean and environmentally friendly production. Innovative startups are also in the group that enjoys this incentive, creating a solid foundation for new projects. In addition, some businesses that convert from sole proprietorships to companies may also be considered for tax exemption, if they meet the conditions prescribed by the tax authority.

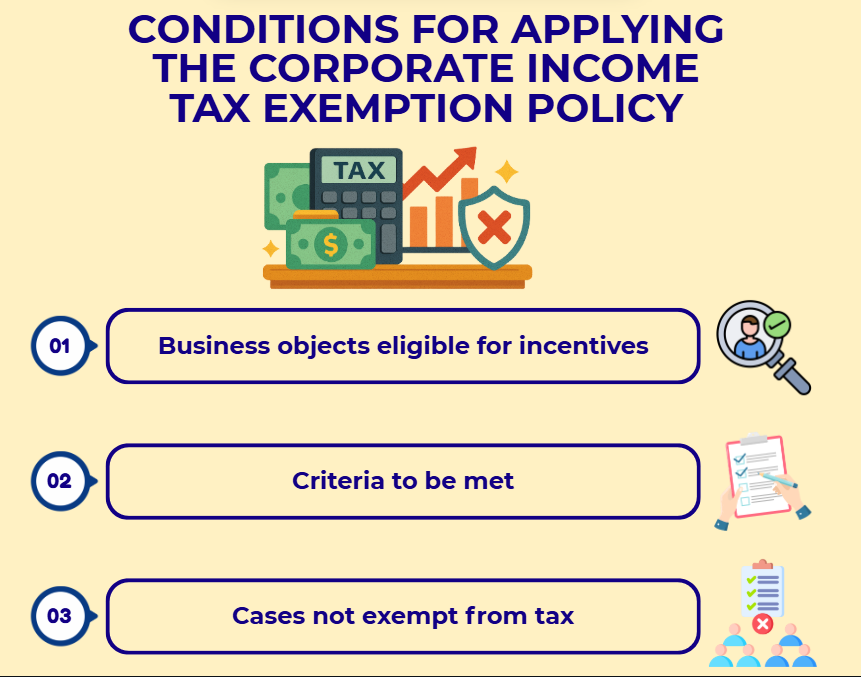

Conditions for applying corporate income tax exemption policy

1. Enterprises eligible for incentives

According to the Law on Support for Small and Medium Enterprises 2017, Article 4 – Criteria for determining small and medium enterprises:

Small and medium enterprises include micro enterprises, small enterprises and medium enterprises, with an average number of employees participating in social insurance of no more than 200 people per year and meeting one of the following two criteria:

a) Total capital does not exceed VND 100 billion;

b) Total revenue of the previous year does not exceed VND 300 billion.

According to Decree 80/2021/ND-CP, Article 5 – Detailed criteria by enterprise size & sector:

Micro enterprises:

– Industry, construction, agriculture, forestry and fishery sectors: Employees ≤10 people, revenue ≤3 billion or capital ≤3 billion.

– Trade and service sector: Labor ≤10 people, revenue ≤10 billion or capital ≤3 billion.

Small enterprises:

– Industry, construction, agriculture, forestry and fishery: Labor ≤100 people, revenue ≤50 billion or capital ≤20 billion.

– Trade and service: Labor ≤50 people, revenue ≤100 billion or capital ≤50 billion.

Medium enterprises:

– Industry, construction, agriculture, forestry and fishery: Labor ≤200 people, revenue ≤200 billion or capital ≤100 billion.

– Trade and service: Labor ≤100 people, revenue ≤300 billion or capital ≤100 billion.

2. Criteria to be met to apply for tax exemption policy

To enjoy the first 3 years of corporate income tax exemption policy, enterprises must meet the following criteria:

– Legal registration: enterprises must have a business license issued by the business registration authority.

– Actual operations: enterprises must have real production and business activities, have transparent accounting books and demonstrate valid revenue and expenses.

– No violations of the law: enterprises must not seriously violate tax, environmental or labor regulations during the tax exemption period.

– Valid business lines: operating in fields encouraged by the state or not on the list of restricted or prohibited businesses.

3. Cases not eligible for tax exemption

Not all new enterprises are eligible for tax exemption incentives. The following cases will be excluded to ensure fairness, avoid taking advantage of policies and encourage businesses that truly start up and contribute to economic development:

– Newly established businesses that are actually split, merged or consolidated from old businesses.

– Businesses that change their name and legal representative but still maintain the same production facilities.

– Businesses operating in industries that have negative impacts on the environment and public health.

– Organizations that are not transparent about their capital sources or show signs of taking advantage of policies to evade taxes.

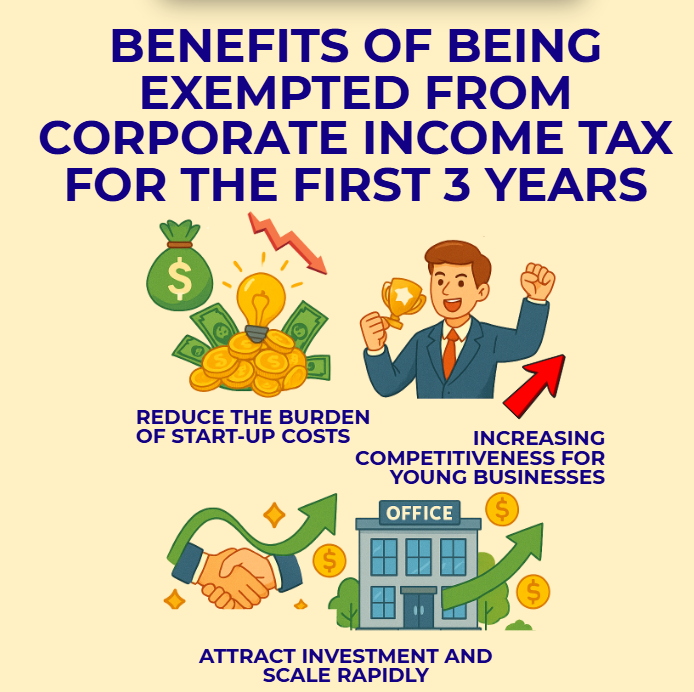

Benefits of being exempted from corporate income tax for the first 3 years

1. Reduce the burden of start-up costs

In the early stages, businesses often face difficulties with capital, operating costs, and competitive pressure. The corporate income tax exemption policy for the first 3 years significantly reduces the financial burden, helping businesses focus resources on production, marketing, and market expansion.

Not having to pay taxes in the first 3 years means that the business’s cash flow is retained and quickly reinvested in essential activities. This is of great significance to startups with limited capital.

2. Increase competitiveness for young businesses

The tax exemption policy helps young businesses have more competitive product prices compared to competitors. When they do not have to bear additional tax costs, they can offer better prices, increasing their ability to capture the market.

In addition, tax exemption creates a cash flow advantage, helping businesses be more flexible in product development, expanding distribution channels, and improving service quality.

3. Attract investment and expand quickly

A new business that enjoys tax incentives will easily attract investment capital from funds or partners. Investors often prioritize businesses with a clear legal foundation and support from the state.

During the 3-year tax exemption, businesses can use retained profits to expand, hire more staff, invest in technology, thereby creating a sustainable advantage.

The policy of exempting corporate income tax for the first 3 years for newly established companies from 2025 is an important turning point in supporting young businesses. Not only does it help reduce financial pressure during the start-up phase, the policy also contributes to creating a fair business environment, encouraging innovation and long-term investment.

Businesses need to proactively seize this opportunity, prepare transparent documents and clear development plans to maximize the benefits that the policy brings.

For any inquiries, contact Wacontre Accounting Services via Hotline: (028) 3820 1213 or email info@wacontre.com for prompt assistance. With a team of experienced professionals, Wacontre is committed to providing dedicated and efficient service. (For Japanese clients, please contact Hotline: (050) 5534 5505).